Tiếng Việt

Tiếng Việt

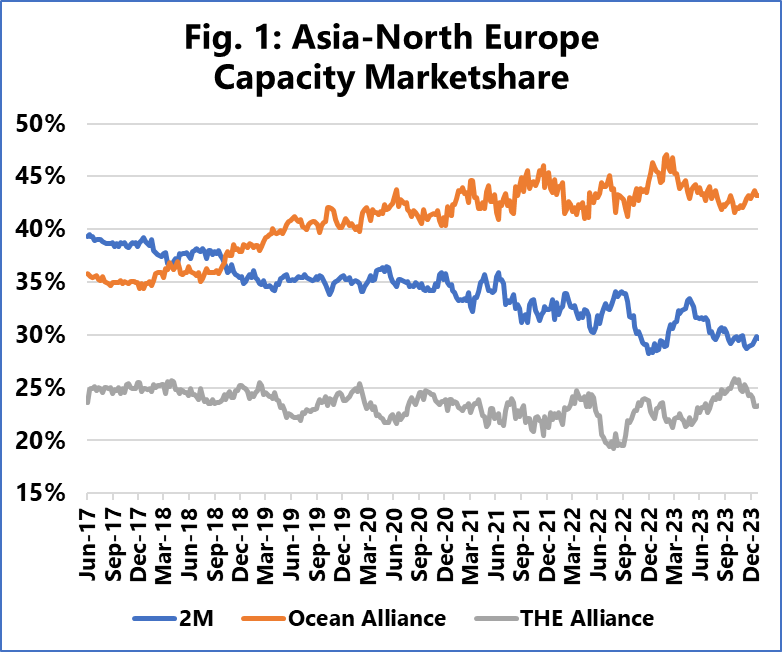

The report by Sea-Intelligence, a Danish maritime data analysis company, provides insights into the fluctuations of capacity market shares among the three major carrier alliances across various trade lanes. Capacity market share refers to the proportion of total capacity operated by each alliance in a specific trade lane.

During the pandemic, there was a notable shift in the Asia-North America West Coast trade lane. The collective market share of the alliances diminished as non-alliance capacity was extensively utilized. The Ocean Alliance, however, managed to recover its market share in 2023, unlike the 2M Alliance, which now stands at a lower position than before the pandemic.

In the Asia-North America East Coast route, the 2M Alliance lost a significant portion of its pre-pandemic gains. Concurrently, both the Ocean Alliance and THE Alliance also experienced reductions in their market shares compared to their pre-pandemic standings.

Nguồn: Sea-Intelligence.com, Sunday Spotlight, số 640

Nguồn: Sea-Intelligence.com, Sunday Spotlight, số 640

A different trend was observed in the Asia-Mediterranean trade lane. Here, THE Alliance slightly increased its share during the pandemic. Alongside the decline of the Ocean Alliance in this lane, both alliances are now nearly at par, trailing behind the 2M Alliance.

The most significant change, as highlighted by Alan Murphy, CEO of Sea-Intelligence, occurred in the Asia-North Europe trade lane. THE Alliance maintained a steady presence throughout the analyzed period. In contrast, the 2M Alliance saw a continual decline in its share, which was captured by the Ocean Alliance. This trend, extending over a significant period, is not directly related to the recent dissolution of the 2M Alliance. Instead, it underscores the growing dominance of CMA CGM, COSCO, and Evergreen in the North Europe route, to the relative detriment of Maersk and MSC.